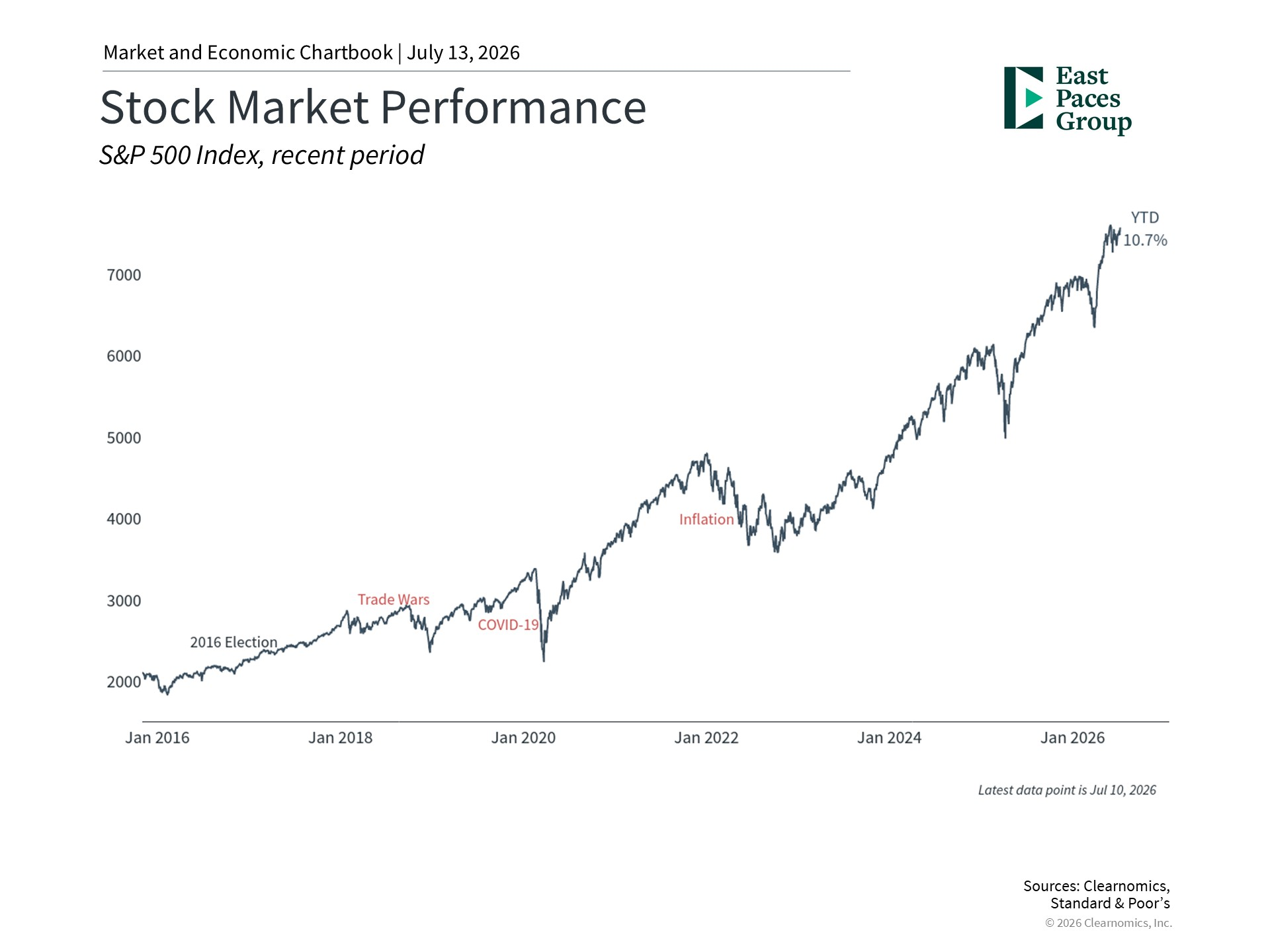

Mid-Year Outlook 2026: Staying Focused as Markets Reach New Highs

A RESILIENT FIRST HALF

INVESTOR TAKEAWAY Major headlines have repeatedly interrupted the market’s advance, but disciplined investors have continued to benefit from staying invested.

The first half of 2026 reinforced a familiar lesson: markets can advance even when the news feels unsettling. Geopolitical conflict and volatile energy prices lifted inflation, while uncertainty surrounding Federal Reserve policy persisted. Even so, the S&P 500 gained 10.7% through July 10 and returned to record territory.

The underlying data has been stronger than the headlines suggest. The economy continues to expand, consumer and business activity remain supportive, and corporate earnings have held up. Investment linked to artificial intelligence is also creating demand across technology, industrials, utilities and infrastructure. At the same time, high valuations and concentrated leadership leave less room for disappointment.

For long-term investors, the goal is not to predict every headline. It is to hold a portfolio that can participate in growth while remaining resilient when leadership changes or volatility returns.

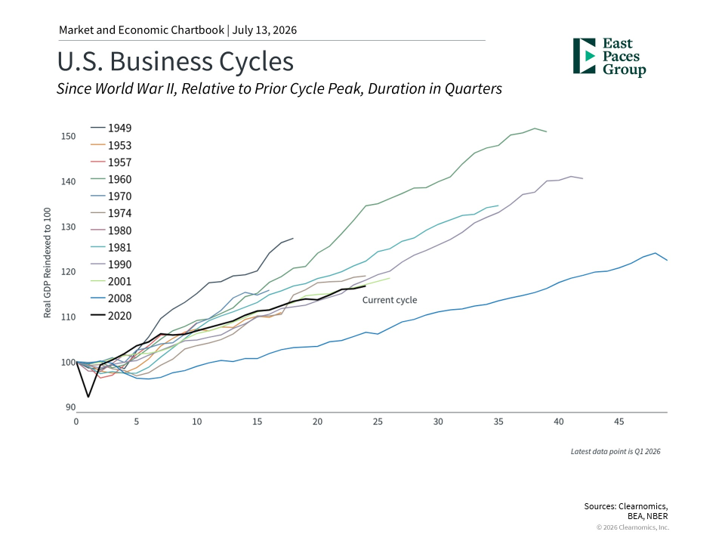

THE ECONOMY REMAINS RESILIENT, EVEN AS INFLATION STAYS UNEVEN

The expansion has endured, but energy prices continue to distort the inflation picture.

INVESTOR TAKEAWAY The current expansion has been steadier than many investors expected and remains within the range of prior long-lasting cycles.

RESILIENCE BENEATH MIXED SIGNALS

The National Bureau of Economic Research dates the latest recession trough to April 2020, placing the current expansion in its seventh year. Bureau of Economic Analysis data show that consumer spending and business investment have continued to support growth, while productivity and corporate profits remain constructive. The path has not been uniform, and softer areas may persist, but the broader economic backdrop remains more resilient than many investors anticipated.

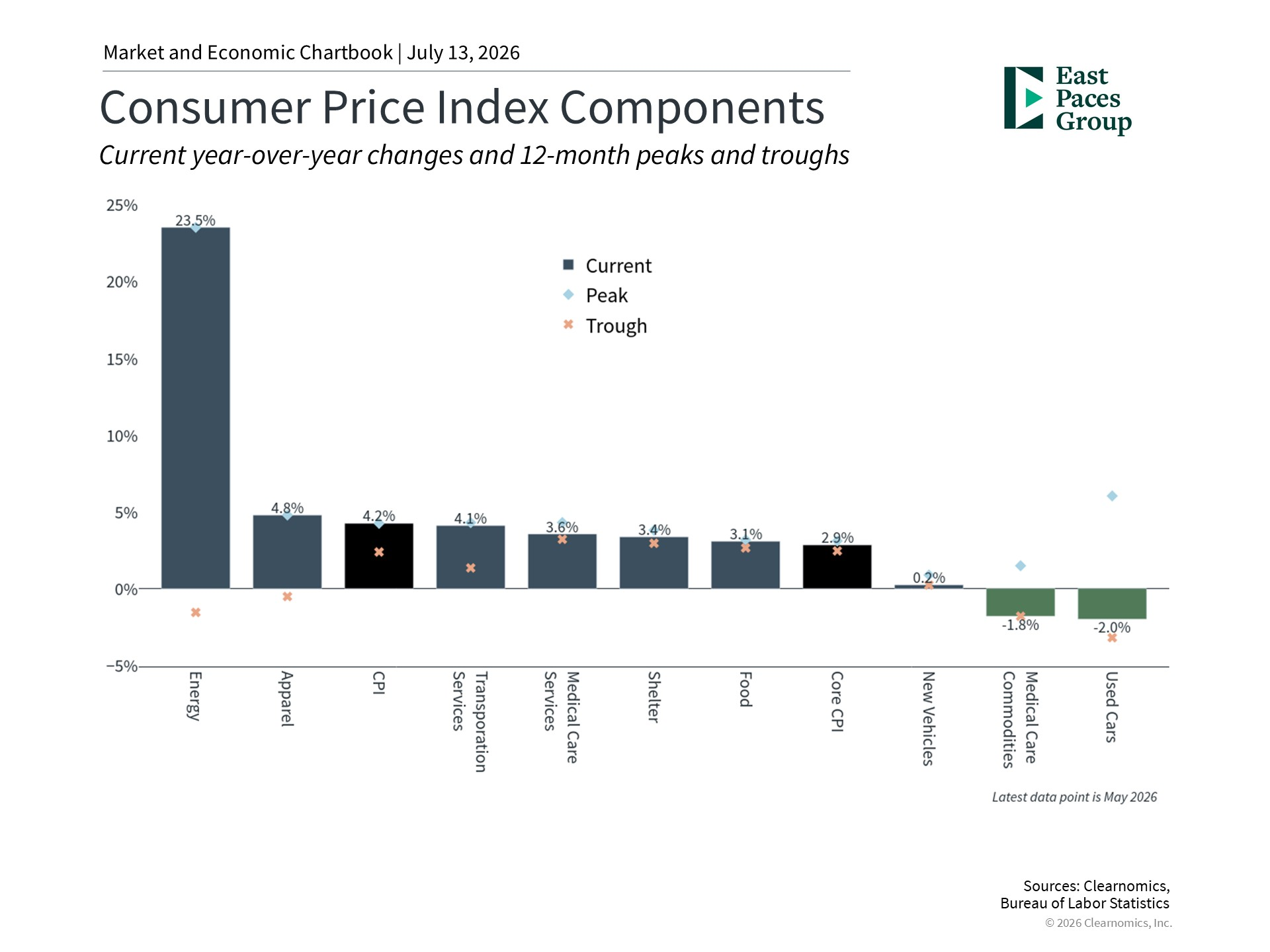

INFLATION REQUIRES PERSPECTIVE

The May CPI reading reached 4.2%, but Bureau of Labor Statistics data show a more nuanced picture beneath the headline. Energy was the clear outlier, while medical, commodities, and used cars declined and core CPI remained below the headline rate. Energy Information Administration data will be important in determining whether lower oil and gasoline prices ease headline inflation. Federal Reserve policy is therefore likely to remain highly dependent on incoming inflation and labor-market data.

INVESTOR TAKEAWAY Headline CPI is elevated, but the pressure is highly concentrated: energy is up 23.5%, while core CPI is 2.9%.

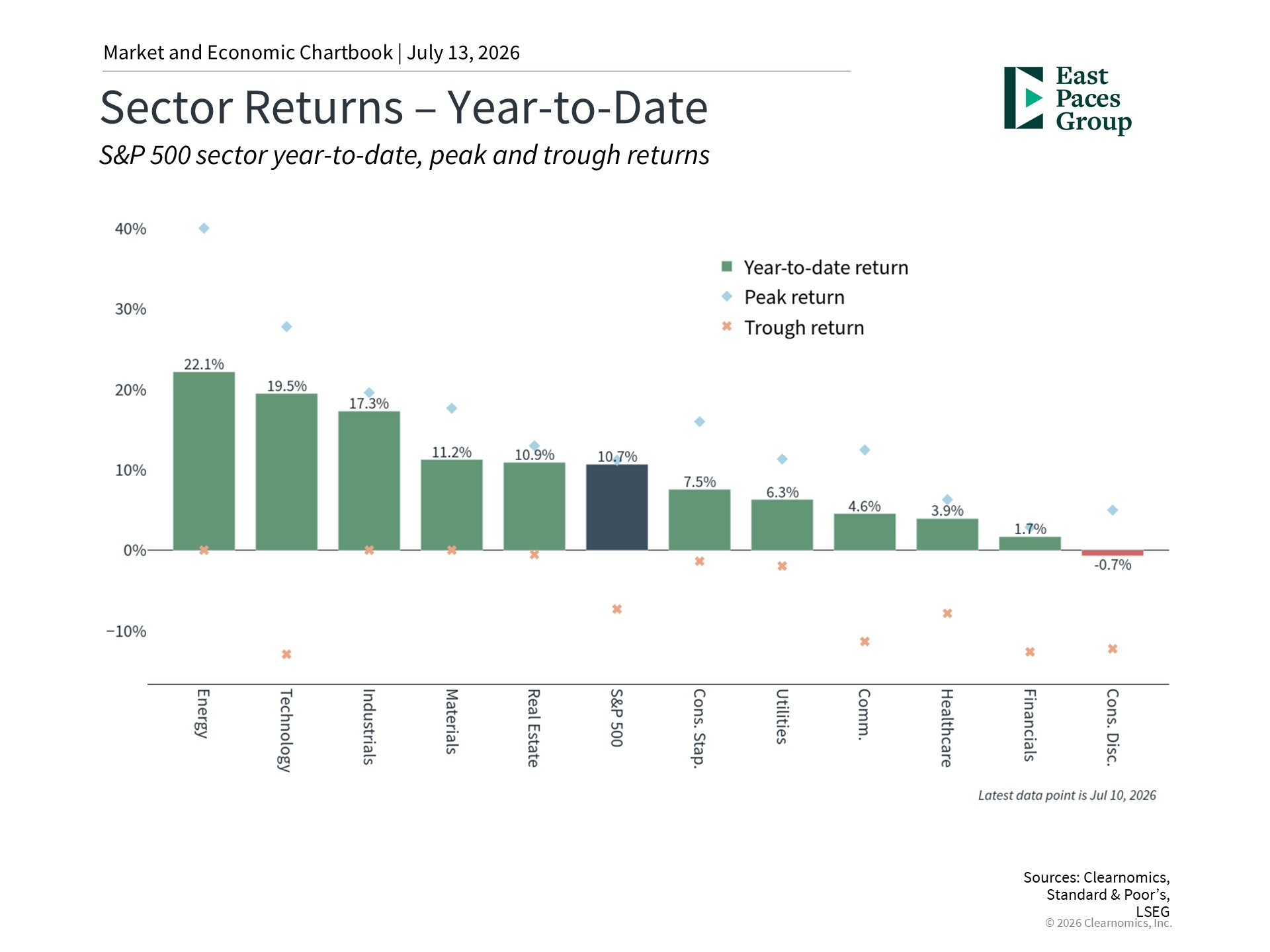

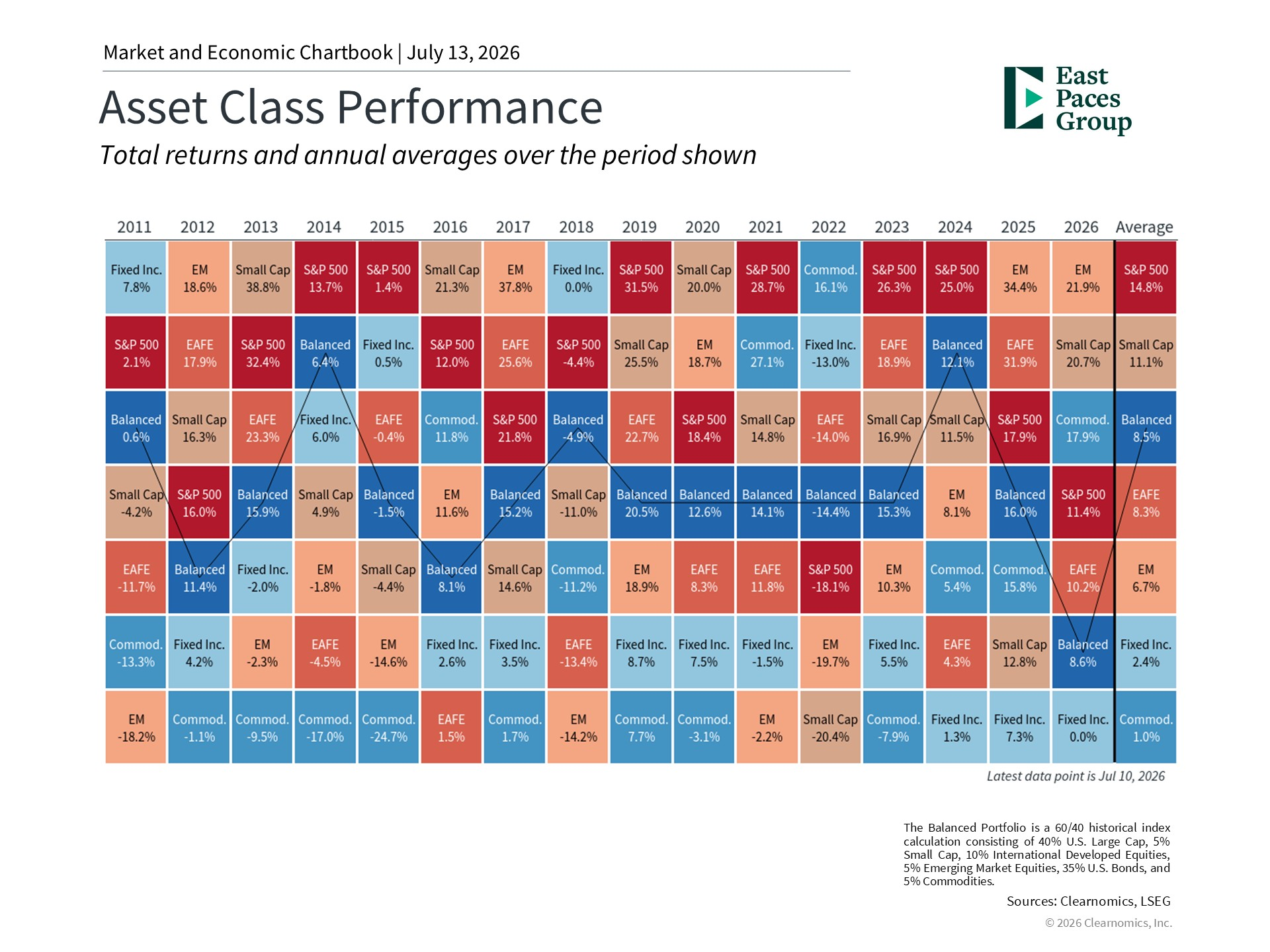

Strong Returns Have Broadened, but Concentration Still Matters

Sector leadership and global performance argue for participation without abandoning diversification.

INVESTOR TAKEAWAY The rally is not limited to a single group: energy, technology, industrials, materials and real estate have all posted double-digit gains.

EARNINGS AND INVESTMENT REMAIN THE FOUNDATION

AI-related investment remains an important market theme, but the opportunity extends beyond the largest technology platforms. LSEG earnings data and S&P sector performance show strength across semiconductors, industrial equipment, utilities and data-center infrastructure. These fundamentals are meaningful, but elevated expectations increase the cost of disappointment. Future returns will depend on which companies convert investment into durable revenue, margins and free cash flow.

DIVERSIFICATION IS NOT A BEARISH CALL

Owning international equities, value-oriented businesses, smaller companies and high-quality fixed income does not require a negative view of U.S. growth stocks. MSCI, FTSE Russell and Bloomberg index data show that leadership rotates across regions, styles and asset classes. The objective is to participate in powerful long-term trends while reducing dependence on one sector, region or economic outcome.

INVESTOR TAKEAWAY No asset class leads every year. The strongest case for diversification is the persistent unpredictability of annual winners and laggards.

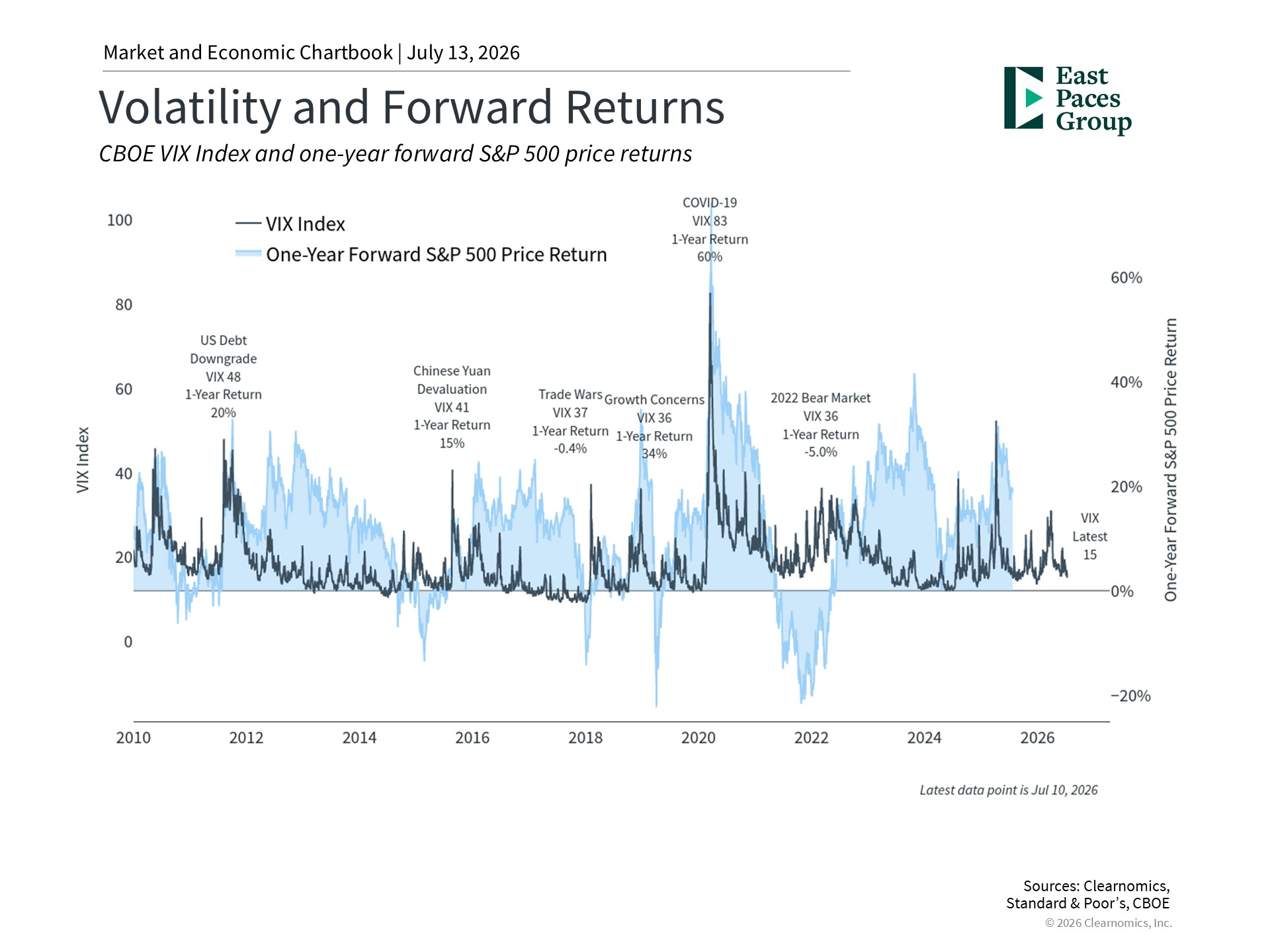

Volatility Is Part of the Journey, Not a Reason to Abandon the Plan

The most important risk is often not the market’s movement, but the investor’s reaction to it.

INVESTOR TAKEAWAY Periods of elevated fear have often been followed by positive one-year returns, although the timing and magnitude of recoveries are never certain.

WHAT WE ARE WATCHING IN THE SECOND HALF

· Whether company earnings and estimates continue to validate elevated valuations, particularly across AI-related industries.

· Whether oil and gasoline prices ease enough to bring headline inflation lower and improve the interest-rate outlook.

· Whether market leadership broadens further beyond the largest growth companies and across global markets.

· Whether investors use volatility to rebalance thoughtfully rather than making all-or-nothing market-timing decisions.

THE BOTTOM LINE

The first half of 2026 rewarded investors who stayed invested and maintained balance. The second half will bring new headlines and periods of uncertainty, but the core principles remain unchanged: align the portfolio with long-term goals, diversify across return drivers, rebalance when appropriate and avoid allowing short-term emotion to override a well-constructed plan.

Sources & Important Notes

Primary economic sources: U.S. Bureau of Labor Statistics; U.S. Bureau of Economic Analysis; Board of Governors of the Federal Reserve System; Federal Reserve Bank of St. Louis (FRED); National Bureau of Economic Research; and U.S. Energy Information Administration.

Market and index sources: S&P Dow Jones Indices; Cboe Global Markets; MSCI; Bloomberg Index Services Limited; FTSE Russell; LSEG; and Investment Company Institute.

Chart compilation: Clearnomics, Inc. Data dates and chart-specific source attributions are shown on each chart.

This material is provided for informational purposes only and is not intended as investment, tax or legal advice or as an offer to buy or sell any security. Indexes are unmanaged and cannot be invested in directly. Diversification does not ensure a profit or protect against loss. Past performance does not guarantee future results. The views expressed are current as of the publication date and may change without notice.